In April, we took a deep dive into the European assets of two of our top 10 portfolio holdings: one is a diversified investment group that owns the world’s largest cruise port operator running 27 ports in 14 countries, and the other is a leather goods manufacturer that counts the world’s most prestigious luxury brands as its clients.

Both companies are from Turkey, and given the abundance of macro noise when it comes to the Turkish economy, especially heading into what promises to be a highly contested presidential election this May, we wanted to see with our own eyes our companies’ assets located outside Turkey and assess their ability to generate substantial earnings denominated in euros and dollars. We were not disappointed.

Ivan Nechunaev and Burton Flynn from the Evli Emerging Frontier Fund went on a mission to deep-dive foreign assets of two large portfolio holdings headquartered in Istanbul.

World’s largest cruise port operator: One of a kind

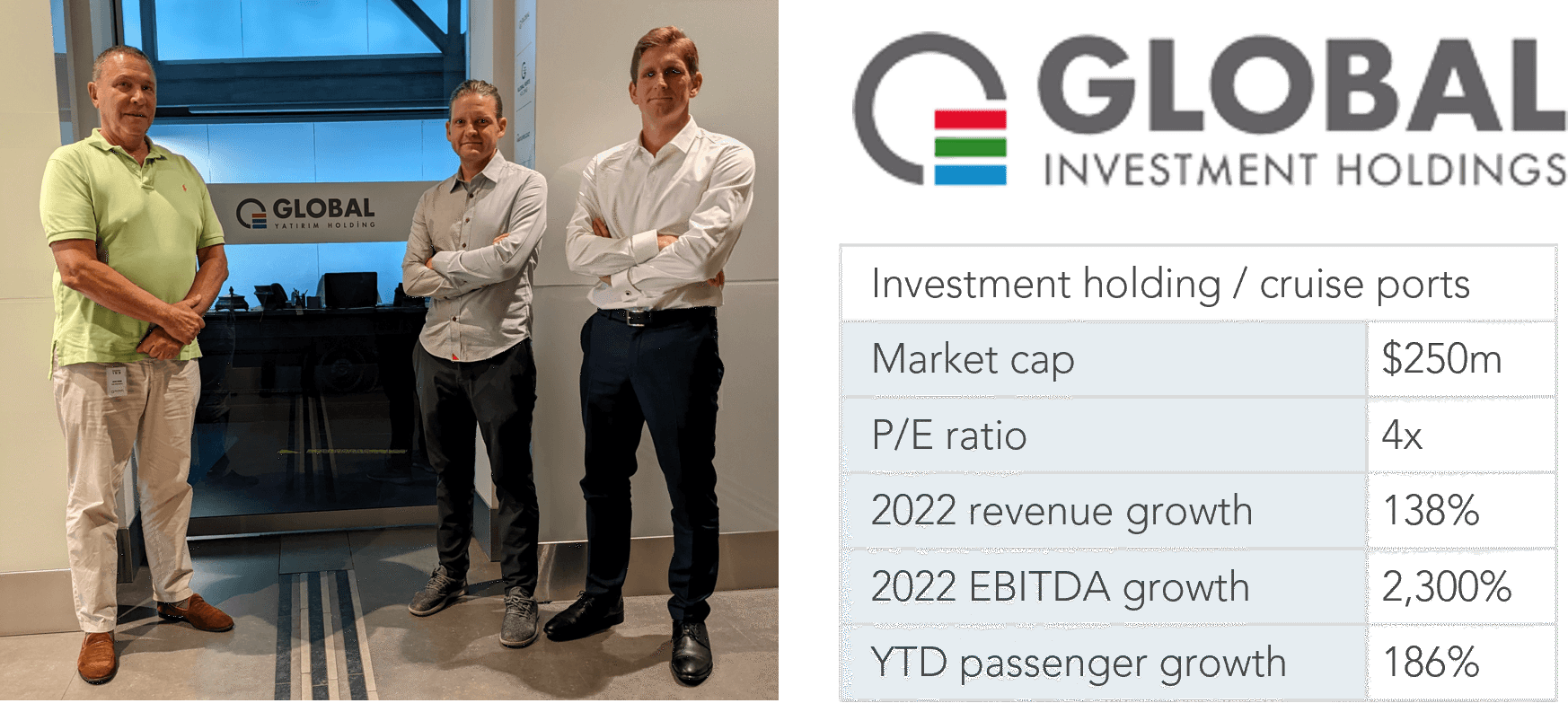

The first portfolio company whose assets we due diligenced in detail on this trip was a USD 250 million diversified investment holding headquartered in Istanbul whose stock trades at only 4x LTM P/E. The group owns six growing subsidiaries ranging from gas and renewable energy to financial services and real estate, but the most prized asset in its portfolio and the chief focus of our research is the world’s largest cruise port operator which manages 27 ports across 14 countries – a highly profitable business with an EBITDA margin of over 70%, whose market cap is only USD 135 million.

The darling of the founder-owner CEO, this cruise port business is one of a kind: there are no other comparably large cruise port operators, as most cruise ports are typically managed by local governments or, less frequently, by the cruise lines. The roll-up strategy of combining all ports into one holding not only helps present a strong partnership proposition to the governments when bidding for 15-to-30-year operating concessions as governments do not have an expertise in profitably running cruise ports, but also allows for cross-pollination of knowledge among the company’s executives managing different ports who gather regularly to share their know-how. Being an independent operator further helps avoid a favoritism bias that occurs when cruise lines manage public ports but favor their own ships.

Meeting with the CEO of a USD 250 million diversified investment holding that owns the world’s largest cruise port operator on our recent Turkey visit.

Cruising on all cylinders

To analyze the cruise port assets of our Turkish holding in particular and the current state of the global cruise industry as a whole, there was no better way than getting on a cruise ship ourselves. Unfortunately, there is no Finnish cruise line we could use for our research voyage, and so we had to stick with another Nordic-sounding brand – Norwegian (which is actually an American company).

In nearly two weeks of cruising, we toured and met with the management of four ports managed by our portfolio company – Barcelona, Catania, Bar, and Venice – as well as nine other ports run either by local governments or by cruise lines. The prevailing sentiment we captured from all our meetings and port visits on the ground – as well as observations at sea – was that the expected number of ships and passengers at cruise ports this year by far surpasses the 2022 and even the pre-pandemic 2019 figures, while docking fees are set to increase after multi-year freezes. These exceptionally strong tailwinds bode well for our port-folio company.

There is no better way to research multiple cruise ports and the global cruise industry than getting on a cruise ship.

Unleashing on Europe’s largest cruise port

Our first port visit was in Barcelona, Spain – the largest cruise port in Europe and one of the top 10 ports globally with a capacity of over 3 million passengers per year. Of the total five terminals in Barcelona, our portfolio company manages three; however, despite running such a large port, the operating team is very lean and efficient with fewer than two dozen full-time employees (this certainly helps attain those 70%+ EBITDA margins).

The head of operations of the port shared with us that his office has been very busy this past winter, refurbishing terminals and opening new shops just in time for the high season (April to October) as hundreds of thousands of tourists “unleash” on the Catalan city of Antoni Gaudi. We also learned that what used to be known as the “low” season (November to March) is not so low anymore as the demand for cruise travel has been extraordinarily strong: in the past years, there would only be 1-2 ships calling at the port in January, while this January there were 15.

The cruise port is expected to exceed 2019 results this year both operationally and financially on the back of greater passenger numbers; additionally, the port authority is about to approve favorable tariff increases for the first time in many years, pressured by inflation and convinced by enormous travel demand and our company’s investments into the port facilities.

.jpg)

On our tour of the largest cruise port in Europe with the head of operations.

Make Sicily great again

The CEO of the second port of our portfolio company which we visited – Catania in Sicily – was equally upbeat about the 2023 prospects, expecting a “very strong recovery” from the pandemic with more passengers arriving than in 2019 and with higher ancillary income thanks to enhancements in the passenger shopping experience at the cruise terminal. Like in Barcelona, the port authority is also working on increasing the docking tariffs as a result of inflation and our company’s significant investments to revamp the cruise terminal.

The operating concession for this sizable port which can dock three large cruise ships at a time expires in 5 years. With a new general manager who joined six months ago with a very strong experience in shipping, cruises, and private infrastructure projects, our company wants to extend the concession, build a new terminal, and operate this growing port for years to come.

.jpg)

On our tour of Catania port in Sicily with the head of operations.

Drinking at a Bar in Montenegro

Our third portfolio visit was Bar in the picturesque Montenegro where we met with the CEO of the Port of Adria and enjoyed locally made Turkish coffee as well as tea from the Turkish mountains. This port is a legacy holding: the group acquired the 30-year operating concession in 2013 as the first port outside Turkey when there had not yet been a plan to evolve into a large cruise operator, and it originally served exclusively as a commercial port. The cruise business was added in 2016 and has kept developing rapidly: this year’s expected increase in the number of passengers compared to 2019 is nearly 80%, while next year’s forecast growth over 2023 is more than 60%.

However, the commercial operations such as container shipping and general cargo still generate the vast majority of this port’s revenue, and in line with the group’s recent strategic review it no longer fits within the holistic cruise port roll-up strategy. Thus, this valuable business with 295 employees, 11 warehouses, forklifts, trailers, and tractors is up for sale to raise cash for new investments that better match the company’s vision.

Meeting with the head of the Port of Adria in Bar, Montenegro.

Back to the roots in Venice

Venice was the fourth and last port of our portfolio company which we visited on this research cruise. Our portfolio company owns a minority stake in this port business as part of a consortium which includes major cruise lines; it has a board seat but is not as actively involved in the port’s daily operations as in its other ports. However, it still stands to collect the benefits of the post-pandemic travel boom: the management of the port expects the number of ships visiting Venice to triple this year compared to last year, as major cruise lines (and their passengers) express heightened demand for the unique beauty of the city of Marco Polo, our legendary Venetian predecessor who traveled to Asia and the Middle East a few (hundred) years before we did.

This growth is promising, given that the entire business model for the Venice port had to change in 2019 after an accident when a large cruise ship damaged a river boat and crashed into the city, which caused the government to ban cruise ships from entering Venice. As a consequence, the cruises now have to dock at smaller ports nearby, or at sea, and the passengers then get transported to the Venice cruise terminal by buses or small boats to go through security and passport control (and to shop at the terminal’s stores). The cruise passenger numbers in Venice are still lower than in the pre-2019 era but the current model is more sustainable for the preservation of the city, and the cruise lines are adjusting their operations accordingly.

.jpg)

Meeting with the management of the Venice port.

The value of an independent private operator

It was easy to notice on this trip that the port terminals operated by our portfolio company were better equipped and managed than the terminals operated by the local governments, and they were generating higher returns on investment, confirming the value which an experienced private independent port operator can provide to public clients across the globe. We had the same observation in the Kusadasi port near Izmir last September, and next month we plan to visit Nassau for the grand opening of its renovated cruise port – top 5 in the world with a capacity up to 7 million passengers per year – in which our portfolio company invested nearly USD 300 million over the past few years and which has been setting passenger number records almost every week this year.

Fun fact: the amount of the Nassau investment alone is larger than our entire Turkish holding’s current market capitalization on the Istanbul stock exchange and twice as large as its cruise port subsidiary’s listing which trades in London.

Learning about all the profit-generating ancillary opportunities at cruise port terminals.

Spending pension savings on a cruise

When investors and analysts discuss the aging population in developed countries, they typically mention healthcare as the industry that will benefit the most from this trend. What we observed was that cruises are particularly popular among retiring baby boomers, and over 80% of cruise passengers tend to be from wealthier countries like the US. In our view, the cruise industry, and cruise ports by extension, is also a business that benefits a lot from the trend of aging: older wealthier citizens want to travel the world (especially now after the pandemic) to gain memorable life experiences by way of spending their pension savings both at sea on the cruise ship and on the ground visiting tourist attractions.

There is no shortage of entertainment on cruise ships, particularly when it comes to popular music from 1960s and 1970s targeted at especially frequent cruise goers.

Stock for the long run

As we were visiting the four ports of our portfolio company and nine third-party ports, it often felt like a broken record: everyone everywhere was telling us how huge the growth in cruise passenger numbers has been since the middle of last year, and how it shows no signs of slowing. We also experienced it ourselves: our ship was booked at over 100% capacity, and it was the same for all other ships at the ports we docked at. Even the famous Wharton professor Jeremy Siegel (author of Stocks for the Long Run) said in a recent interview that he was about to go on a cruise!

The official cruise industry statistics fully confirm this strong sentiment. What does this mean to us? It means that regardless of the political and economic volatility on the ground in Turkey and the exchange rate of the Turkish lira, our Turkish portfolio company owning the world’s largest cruise port operator will have a very strong growth in dollar- and euro-denominated earnings for the next several quarters. With a nearly 50% discount to the listed subsidiaries’ sum-of-the-parts NAV and an 80% discount to the estimated fair value, this cheap and growing holding is a bargain.

Waters for the cruise industry have been getting particularly good to sail lately.

Made in Italy

When on the cruise, not only did we visit 13 ports, speak to countless contacts on the ground and at sea, and record a podcast from Dubrovnik with the leading Swedish fund platform about how we look for stocks that can double, but we also managed to travel to Tuscany to do due diligence on the assets of another cheap growing high-quality Turkish company in our fund.

This diversified USD 140 million leather goods company headquartered in Istanbul has been in operation for over 50 years and is majority-owned by the founding family. The firm produces and sells leather goods under its own brand both online as well as across over a hundred outlets in Turkey; it sells online under its own brand through Zalando in Europe; it operates dozens of Samsonite franchises in Turkey; it produces leather goods in Turkey for further export to the world’s most prestigious luxury brands in Europe; and it now also starts production in Europe for the world’s most prestigious luxury brands with a label Made in Italy so coveted by the world’s wealthy. The stock trades at only 9x LTM P/E and the company has a large net cash position for various growth initiatives.

Meeting with the CEO of a USD 140 million leather manufacturer on our recent Turkey visit.

The bold movers and the first explorers

The business is managed by a highly capable second generation family CEO with degrees in finance from the US and leather technology from the UK, whose entrepreneurial vision and international mindset help the company boldly expand its business not only in Turkey but also outside Turkey. One such bold move came a few months ago when the company established a factory in Tuscany, Italy.

Typically, a move in the other direction would be more expected: many firms set up factories in manufacturing hubs like Bangladesh or Vietnam. However, in this case, our firm decisively upscaled its profile and visibility and moved closer to its prime clients, right next to their production homebase in the Florence region – the capital of Italian leather making (for example, there is a Gucci museum in Florence which tells the story of leather manufacturing in the region by this renown brand). The closest luxury brand is now only a 45-minute drive from our company.

We wanted to visit this new factory to see it being furnished in real time, and we couldn’t miss the opportunity to make a roundtrip to a beautiful village in Tuscany 2.5 hours from the port of Livorno where our ship docked for 10 hours. Upon arriving at the factory with our business bags made by this company from sustainably sourced Norwegian leather which we bought last September on an unannounced due diligence visit to its store in Antalya and have been using ever since, we were greeted by the company’s CEO. When he told us that we were the very first external visitors at his new facility, we thought to ourselves: “We heard this before.” Over the past 10 years, our fund has often been the very first foreign visitor to multiple emerging markets companies (we also seemed to be the only active foreign investor in Turkey last year, which paid off as our fund’s Turkish holdings generated a 92% return in euro terms).

With the CEO in a village in Tuscany at the company’s sign which was getting erected the day we arrived.

Cutting the edges and reducing Italian unemployment

On our tour of the factory which goes live in early May, we saw a lot of cutting-edge technology – quite literally. The brand new laser cutting machines and leather-making equipment from Japan and Italy reminded us more of our visits to the semiconductor companies in Penang, Malaysia rather than of stereotypical leather workshops! The CEO was proud that his clients and prospects from the world of luxury are very excited about all the new machinery due to its precision and ability to support production of significant volumes of highest-quality leather goods, as opposed to the fully hand-made production which sounds very authentic but does not necessarily mean higher quality and is also very inefficient time-wise. It only helps that thanks to the Italian government’s incentives as part of the Industry 4.0 transition, our company will also be able to recover 40% of its investment in innovative equipment through tax rebates.

Head of the factory who conveniently lives nearby brings a plethora of experience: he was previously running production for brands such as Prada, Yves Saint Laurent, and Armani. The company received an overwhelming demand for the new jobs it created in the village: for example, the hiring rate of new employees relative to the total number of job applications is below 10%, similar to the student acceptance rates at the most elite Ivy League colleges. Despite that the overall unemployment, particularly among youth, is relatively high in many regions of Italy, this particular case revealed an insightful truth: there is a good interest in work but people do not want to leave their home cities or villages and commute for longer than 20 km, and so when work gets delivered to their doorstep they are happy to apply. No wonder the local municipality likes the Turkish newcomer that creates jobs, trains people (the government even pays for that training), and takes good care of them: in fact, our company has built a canteen and new locker rooms with showers on site, and there will be a doctor’s office as well.

Of course, given that the company will manufacture luxury leather goods that may have a price tag higher than a used car, the entire factory is also equipped with special nuanced mechanisms like those seen in the movies to prevent theft and burglary quite common in the industry.

Testing the brand new high-tech leather-making equipment which resembles precision machines from semiconductor plants.

Delighted about Turkish delight

In our meeting with the CEO after the factory tour, overlooking the trademark-worthy hills of Tuscany and symbolically drinking Turkish coffee (this time from Turkey) and eating Turkish delight, we could not help but notice how happy the CEO was with the direction his company is moving. According to the CEO, who travels to the new factory every week from Istanbul, the move westward has truly been a “game changer” for the brand perception and proximity to clients, and the ability to produce with the status label Made in Italy has opened a new chapter in the company’s development. The moment the new factory’s set-up began, the inflow of inquiries from luxury brands for potential production cooperation became “massive” – the CEO has “never seen so many interested parties”, and the company might even need to hire more people than expected on the back of exceptional demand. The timing could not be better, now as the long-expected recovery of China’s luxury market started showing through better-than-expected financial results of publicly listed luxury brands.

We were delighted about what we saw on this factory visit. The fortified foray into the growing global luxury market will provide our company with substantial international growth opportunities, further cementing its dollar- and euro-denominated earnings stream.

Sitting down with the CEO for Q&A with Turkish coffee and Turkish delight after our factory tour.

Going where others don’t

On this deep-dive research voyage we wanted to establish whether our two top-10 portfolio holdings from Turkey have the ability to grow their foreign-currency earnings at a substantial rate through their assets outside Turkey. The answer is a resounding yes.

Both companies are run by bold, smart CEOs who go where others don’t (think creating the world’s largest cruise port operator or establishing production in Italy); both succeed despite volatility back home in Turkey thanks to globally oriented business strategies; both grow earnings at a high rate; both are cheap. We estimate that both have the potential to double earnings this year.

Burton Flynn, CFA

Burton Flynn, CFA

Equity Research, Evli Emerging Frontier Fund

Ivan Nechunaev

Ivan Nechunaev

Equity Research, Evli Emerging Frontier Fund