Each episode of Star Trek started with the mission of the starship Enterprise: “to boldly go where no man has gone before.” This mission resonates with us, since we go where other investors don’t. Dozens of times we have heard an obscure company’s CEO tell us that we are the first foreign investor they have ever met. Indeed, we are often the only foreign fund on a portfolio company's shareholder register. Our portfolio is cheaper, grows faster, and is higher quality than most EM funds, while our average market cap is the second lowest of all listed EM funds in the world. This is the ‘final frontier’ that the Evli Emerging Frontier fund explores.

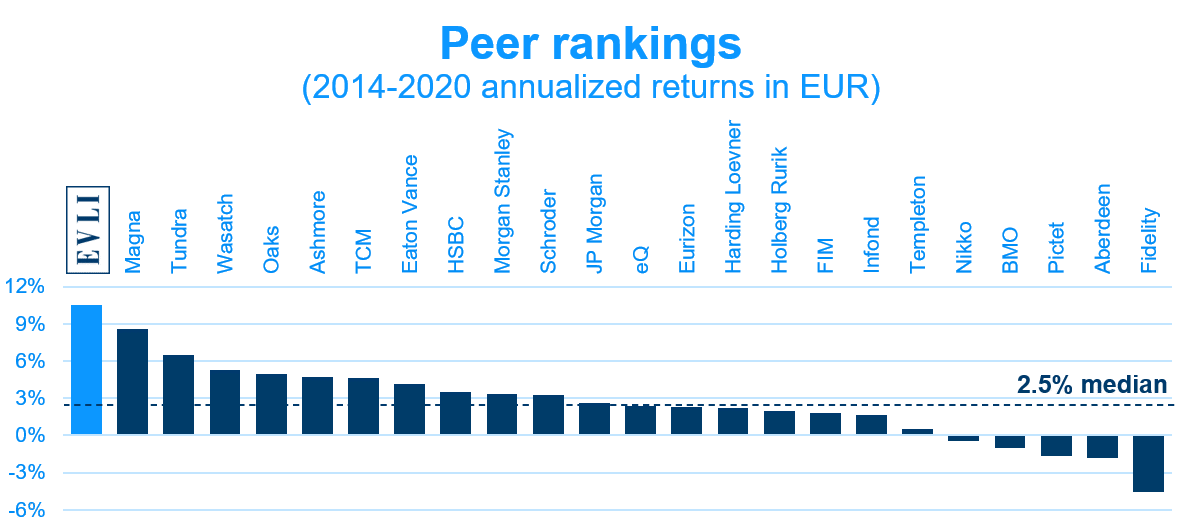

The Evli Emerging Frontier fund has realized a net-of-fees annualized return of 10.5% over the past seven years, ranking #1 among all 24 frontier emerging markets peers listed on Bloomberg.

Source: Bloomberg.

Note: Index used is MSCI Emerging Markets Equal Country Weighted in EUR. Peer ranking includes all listed funds launched before 2014 with more than 50% weight in frontier emerging markets.

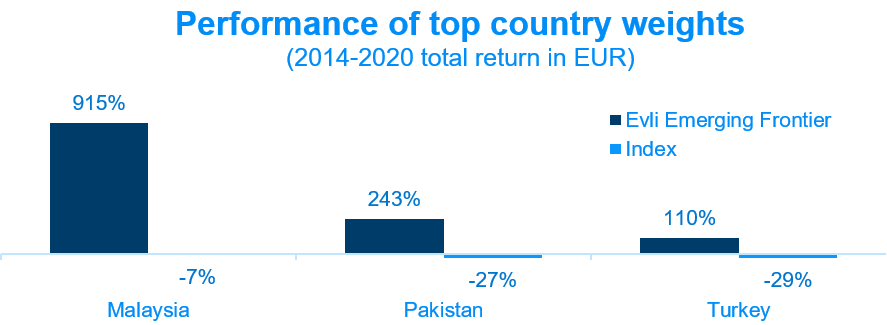

This performance is attributable entirely to the fund's bottom-up stock selection: the indexes of the three markets to which the fund had the largest exposure over the past seven years – Malaysia, Pakistan, and Turkey representing a combined average portfolio weight of 44% – have all lost money. However, despite the difficult markets, these three countries together account for approximately 75% of the fund’s seven-year performance.

Source: Bloomberg.

Note: Indexes used are MSCI Malaysia, MSCI Pakistan, and MSCI Turkey.

Performance should be substantially higher in the next seven years

While the fund's performance over the past seven years may be viewed as impressive in its own right, it was severely restrained by four cyclical headwinds.

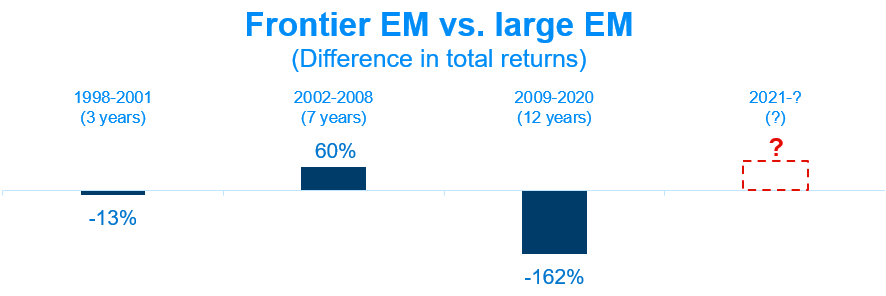

The average emerging market index (80% of which is frontier emerging markets) returned a paltry 2.5% annualized over the past seven years, compared to 8.0% from the mainstream EM index (80% of which is six large emerging we don't invest in). As we wrote in The case for frontier emerging markets, although the smaller EM countries have outperformed mainstream EM over the long run, it works in cycles and frontier emerging markets have been out of favor relative to emerging markets, underperforming by 77% over the past seven years.

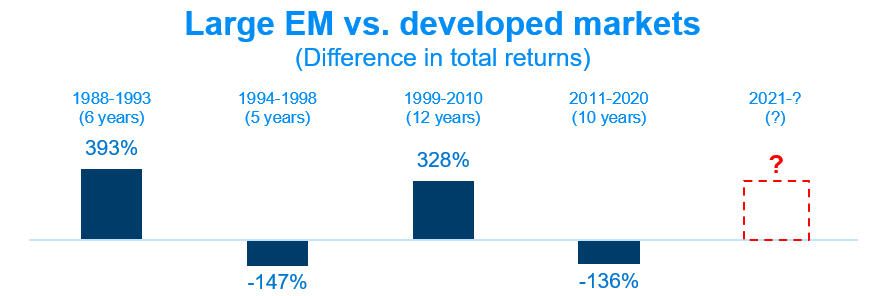

Many would not be impressed by the emerging markets index’s 8.0% return if they consider that developed markets returned 11.1% per year during this time. However, as we wrote in The case for EM, although EM has outperformed developed markets over the long run, it also works in cycles and emerging markets have been out of favor relative to developed markets, underperforming by 41% over the past seven years.

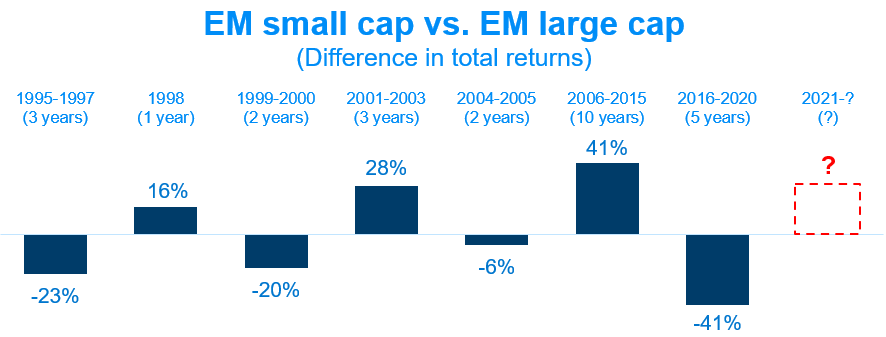

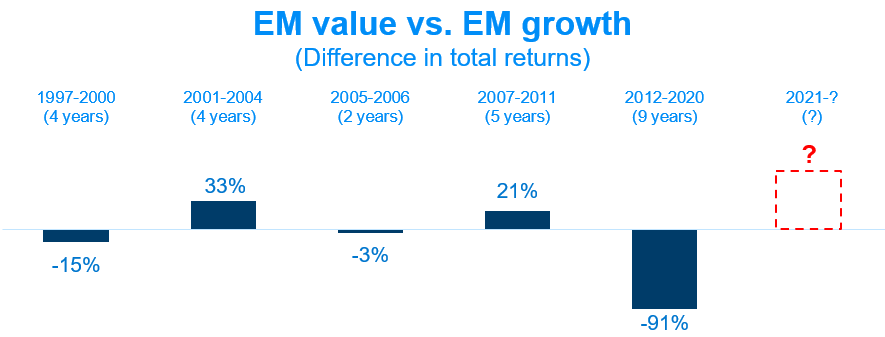

Our fund’s strategy is highly exposed to the small cap and value factors, which are two of the three fundamental factors which predict equity performance over the long run according to the widely used Fama-French three factor model. However, these two factors also seem to work in cycles and EM small cap stocks and EM value stocks have been out of favor relative to EM large cap stocks and EM growth stocks, underperforming by 18% and 65% respectively over the past seven years.

When any of these four cyclical factors turn, we believe our fund’s performance will be even stronger. In the scenario that in addition to successful bottom-up stock selection these four other cylinders start firing at the same time, our returns could be substantially higher.

Source: Bloomberg.

Note: Indexes used are MSCI EM Equal Country Weighted, MSCI Emerging Markets, MSCI World, MSCI EM Small Cap, MSCI EM Large Cap, MSCI EM Value, and MSCI EM Growth.

How we became the top-performing frontier emerging markets fund

In this final part of our “The case for” trilogy, we explain how our highly active 'boots-on-the-ground' approach, deep immersion in the markets, and hyper-focus on performance have helped us produce top returns for our investors.

1. We are one of the only truly active EM funds

Benchmark-agnostic. In The case for frontier emerging markets, we showed that most EM fund managers mimic an index that lacks broad exposure to the developing world. Instead of being constrained by an undiversified benchmark, we roam freely across 50 frontier emerging markets that are severely overlooked by most other funds, searching for the most compelling investment opportunities.

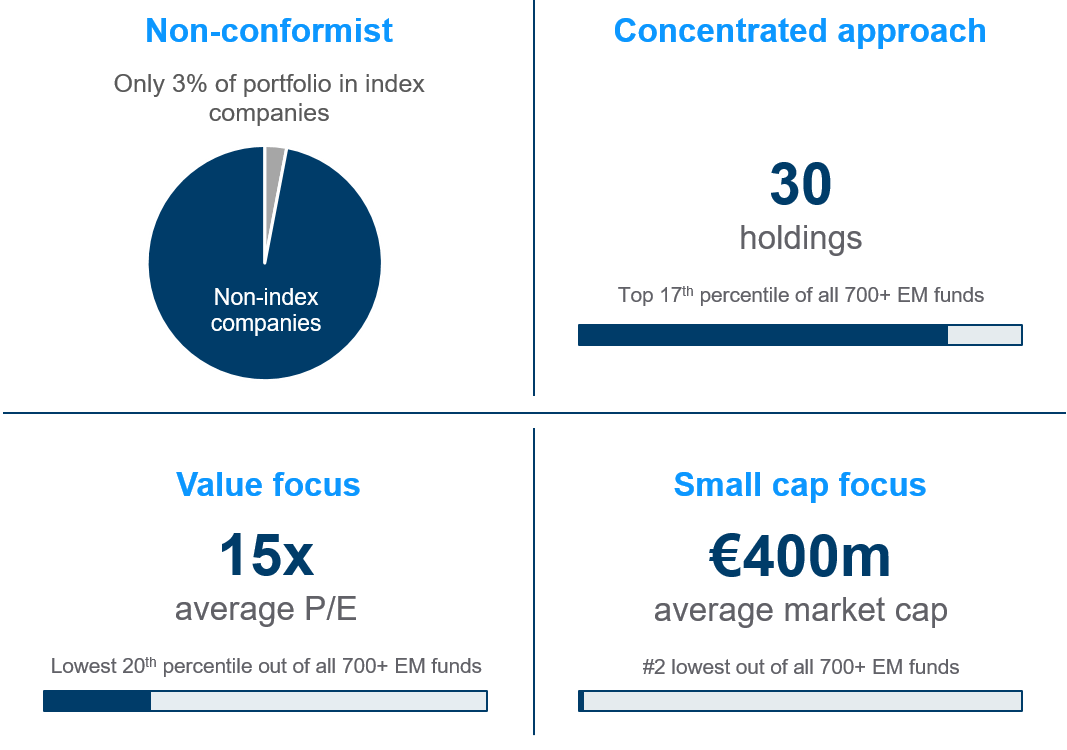

Focus on smaller non-index companies. Our strategy is to look for high-quality growing companies which are cheap: the best of all worlds. In order to find such undiscovered gems, we focus on small companies which are not part of any of the mainstream indexes. Our portfolio’s average market capitalization is €400m, which is the second lowest among all listed EM funds, and only one of our holdings (3% of the portfolio) is found in any of the three leading EM indexes. Also, instead of commodity-linked stocks which comprise the bulk of most emerging markets indexes, we focus on consumption-driven stories benefiting from the emerging middle class.

Concentrated approach. A key aspect to being an active investor is owning only a small number of high-conviction holdings. While it is not uncommon for other funds to hold upwards of 100 stocks, we own larger stakes in fewer portfolio companies in order to better know and more closely monitor our holdings, and to ourselves greater capacity and incentives to proactively engage with management. We currently own 30 positions, with 10 accounting for 50% of our portfolio. By this measure, our fund is more concentrated than 83% of listed EM funds.

Macro risk management. For the first five years of the fund, as bottom-up investors we didn’t consider macro factors in our portfolio construction process. However, after getting burned by the 2018 Pakistani rupee and Turkish lira currency crises, we spent a great deal of time studying how we could avoid such excessive macro risks in the future, and developed a process to investigate potential canaries in the coal mine. As a result, while our portfolio is still primarily a function of where we see the most compelling opportunities, we now proactively impose strict country limits or outright exclusions which have already helped us avoid the 2019 Argentine peso collapse and mitigate the 2020 Turkish lira depreciation.

Proprietary ESG process. Nearly 90% of our hand-picked small-cap portfolio holdings are not rated by third-party ESG data providers. As such, we implement our own proprietary ESG process to identify the most sustainable firms, as well as companies which have opportunities for improvement and whose management teams are willing to engage with us to make positive changes. As part of this process, we ask every company to complete a comprehensive ESG questionnaire. The 108 questions are the result of several months of work and are informed by academic studies, proprietary research, and our own experience in impact investing. We already have evidence that this alternative data can help us generate additional alpha. We also spend a third of each CEO meeting asking questions about the company’s climate change risk management, human capital practices, and minority shareholder attitudes.

Active ownership. In order to help our obscure portfolio companies unlock value, we act as friendly shareholder activists and work with them through a series of engagements, drawing upon our prior EM private equity experience. We provide recommendations aimed at improving their ESG standards, which academic research has found to carry strong potential for alpha generation. In 2020 alone, we made 114 recommendations to 24 firms through 34 separate engagements. We helped our companies publish their first-ever investor presentations and quarterly press releases, initiate earnings calls and investor days, get more sell-side research coverage, improve market access, report carbon emissions, join ESG indexes, and align with UN SDGs. Source: Bloomberg.

Source: Bloomberg.

2. We deeply immerse ourselves in our markets

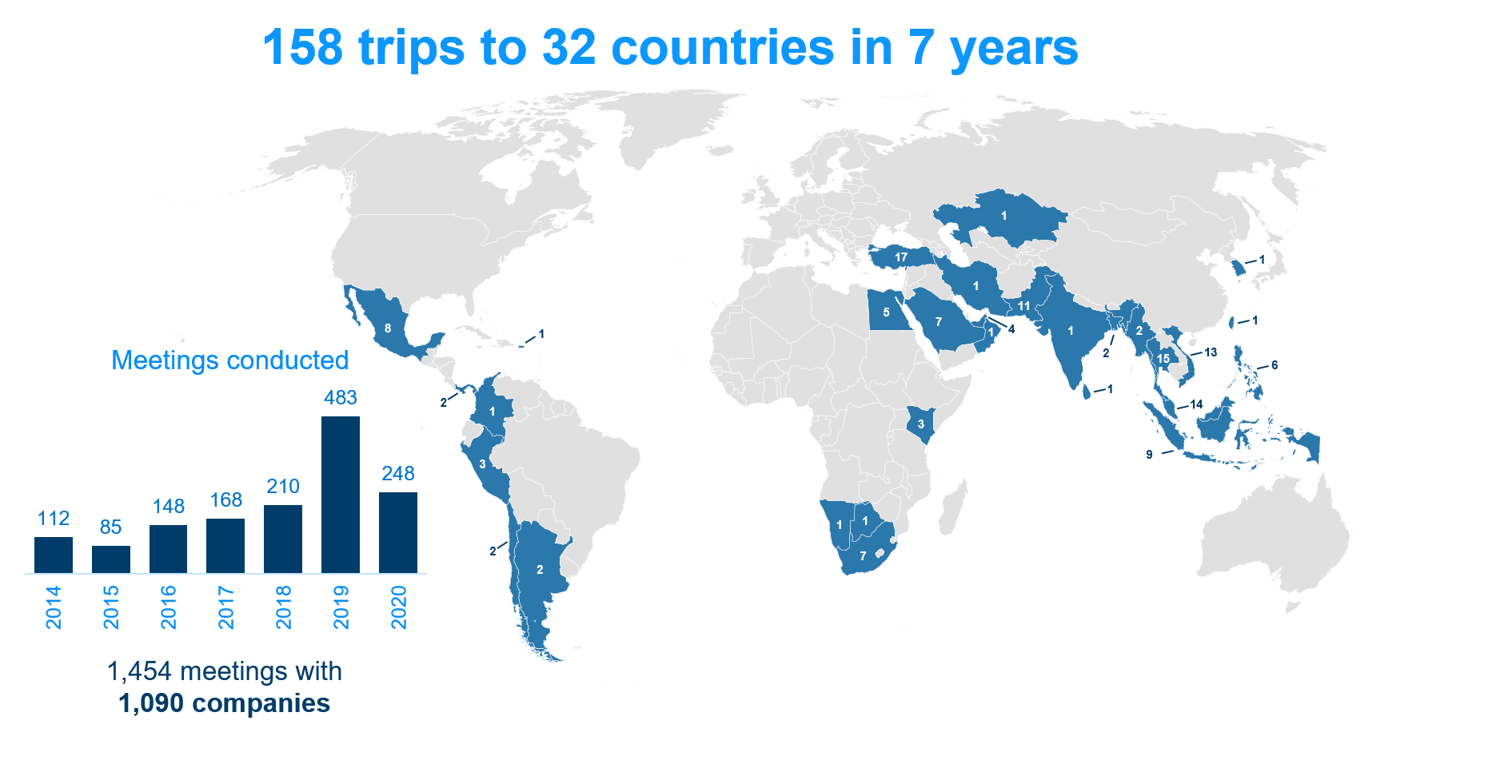

Commitment to meet every company before investing. From the beginning of the fund, we promised our investors that we would never invest in any company unless we met management face-to-face. We like to get to know the people running the businesses we consider owning. As a result, in the past seven years we have conducted 1,500 in-person meetings with the CEOs and other senior executives of over 1,000 companies – all executed by essentially two full-time investment professionals. We are unaware of any other EM fund with such a meeting policy.

Seeing assets first-hand. We find value in the Peter Lynch approach to investing – touring a company’s assets or testing its products – which sometimes helps us corroborate management’s expectations. For instance, a Vietnamese IT distributor’s vast new warehouse facility showed us the company’s capacity to handle the expected rapid increase in demand for their products. On the other hand, an air conditioner parts factory three hours from Bangkok was desolate despite the CEO’s claims of record sales.

Engaging with regulators. We strive to meet with the regulators and policy-makers shaping the local market environment in order to get an authoritative view of macro risks. For example, in the year prior to the pandemic, we met one-on-one with the central bank governor in South Africa, finance minister in Thailand, head of the SEC in Saudi Arabia, president of the stock exchange in Bangladesh, minister of climate change in Pakistan, and commissioner of black economic empowerment in South Africa.

Building local networks. We are constantly building our in-country networks: meeting with local fund managers, analysts, economists, professors, politicians, journalists, and other market experts. This helps us learn more about the economy, run reputation checks, identify controversial ESG issues, and measure local sentiment. Also in the year prior to the pandemic, we connected with fellow charterholders at a CFA society event in Pakistan, talked stocks with a fellow Nordic frontier fund manager in Thailand, exchanged market views with a Malaysian sovereign wealth manager, received advice from the ‘Warren Buffett’ of Indonesia, collaborated with the ambassador of Finland to Vietnam, learned the concept of social business from a Nobel peace prize laureate in Bangladesh, discussed the local property market with a Bloomberg reporter in the UAE, engaged in a friendly debate on sustainability methods with the Africa head of UN PRI in South Africa, and had lunch with a different Wharton alum every day during our month in the Philippines.

Deep dives into our markets. In 2019 we took to the road with our families on a mission to live in 12 frontier emerging markets for one month at a time. In the 10 months before the pandemic abruptly ended our project we met 632 companies face-to-face and had 210 meetings with regulators and local market participants. This month we are embarking on a similar project in which we will attempt to meet 1,000 companies in 11 months, one sector at a time, via a virtual roadshow. We believe these types of projects give us an opportunity to look at companies through different lenses by comparing them with others in the same country or sector.

3. We are hyper-focused on delivering the best results

Dedicated team. Very few investment funds are managed by a team concentrated on a single strategy. Rather, portfolio managers and analysts at ‘product shops’ typically juggle their time between various funds. However, the investment team at Terra Nova Capital is 100% focused on advising only the Evli Emerging Frontier fund.

Ideal environment for successful investment decisions. The boutique arrangement of Terra Nova as Evli’s subsidiary located in Dubai allows us to not only reach most of our markets in less than eight hours, but also be a small team with a flat, entrepreneurial culture free from the distractions of bureaucracy and politics. Warren Buffett believes truly exceptional investment performance can only be achieved when executed by one or two decision-makers – as groups grow their decisions get more homogenized and, just as the law of large numbers predicts, performance becomes closer to average.

Focus on returns rather than asset gathering. Some investors balk at performance fees. But performance fees aren't at the expense of anyone – they are only earned if a fund ‘grows the pie’. Indeed, of the 24 frontier emerging peers with a seven-year track record, five of the 12 top-performing funds charge a performance fee while only one of the bottom-performing 12 does. Charging only a management fee can incentivize managers to grow AUM as much as possible even though larger fund sizes narrow the investment opportunity set and thus limit performance potential. Our performance fee incentivizes us to prioritize returns, even though it means limiting the fund size.

Alignment of interests. The managing partner has invested 100% of his and his wife's eligible assets into the Evli Emerging Frontier fund, and has committed to invest in the fund all dividends he receives from his ownership in Terra Nova Capital. Thus, he is ‘eating his own cooking’ and is personally incentivized to prioritize investment performance. Research shows that for every additional 1% that a manager owns of his or her fund, risk-adjusted performance rises by 3%.

The Evli Emerging Frontier fund investment team in between meetings in Jeddah, Saudi Arabia.

Conclusion

In the first blog of our “The case for” trilogy (The case for emerging markets: It’s about time) we articulated why strong productivity gains and favorable demographics boosted by the right time in the cycle make EM very well-positioned to outperform developed markets in the next several years.

In the second blog of the series (The case for frontier emerging markets: The forgotten fifty), we showed that less-efficient frontier emerging markets offer a truly active fund manager cheaper and faster-growing investment options as compared to mainstream EM, manifesting a tremendous untapped opportunity for both investment performance and diversification.

This final blog makes it clear that a highly active approach can produce superior results regardless of external conditions. Our commitment to being one of the only truly active EM funds in the world, deeply immersing ourselves in the markets, and staying hyper-focused on delivering the best results have led Evli Emerging Frontier to become the highest-performing fund among frontier emerging markets peers over a full investment cycle.

We will continue to explore strange new markets. To seek out cheap, growing, high-quality companies. To boldly go where no investor has gone before.

Learn more about our Evli Emerging Frontier Fund

Our recent blogs

The case for frontier emerging markets: The forgotten fifty

The case for emerging markets: It’s about time

Testing our portfolio for COVID-19: Why we sold Turkey

The value of investor meetings: Five things we learned from interviewing 323 CEOs last year

+1,000% during COVID-19: Protecting our portfolio with Malaysian medical gloves

A month in Turkey: Retreating from coronavirus

A month in South Africa: The road to nowhere

A month in Saudi Arabia: Piercing the veil

A month in Vietnam: Closing the deal

A month in Thailand: Driving three hours to see an empty factory

A month in Pakistan: An altercation at the ministry of finance

A month in Bangladesh: We're investing billions in the world’s best stock market

A month in Indonesia: Offending Trump in Bali

A month in Malaysia: Finding another gem on "Treasure Island"

A month in the Philippines: How active management helped us beat the traffic (and the market)