It’s October, soon Halloween is here and, even though I don’t have kids and know nothing about parenting, I am certain that nothing scares children more than the words “Emerging Markets corporate debt”.

The list of frightening aspects is plentiful:

- There’s Russia’s geopolitical issues.

- Turkey’s coup attempt and downgrade to junk.

- Brazilian corporate and political scandals.

- Presidential candidate Trump’s Mexico obsession.

And then there’s China, for which CNBC and Bloomberg have a favourite term, “China worries”, to lazily explain any down day in global markets when they cannot find any other good reason.

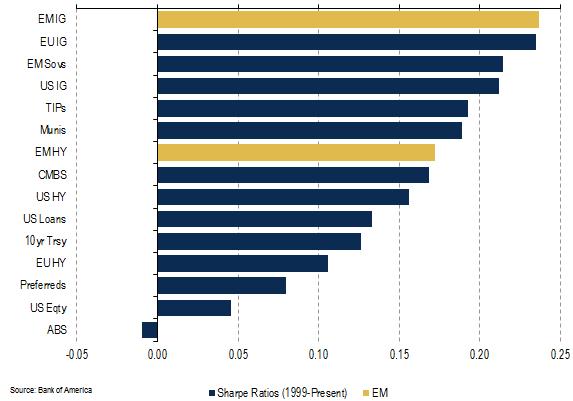

So, EM corporate debt? Who buys this stuff? Well, if you ignore it, you’re missing out on some excellent diversification and the best risk/return over the past 17 years. In fact, since 1999, EM IG has the best risk/return (in terms of Sharpe ratio) among all major fixed income asset classes. And EM HY outperforms its US and EU counterparts by the same measure (see picture below).

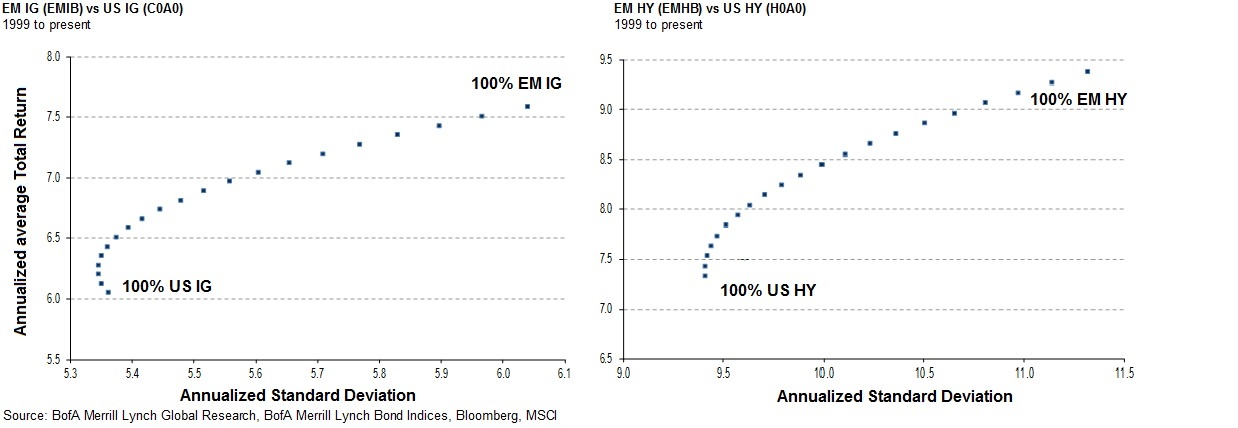

It is interesting that diversification is one of the basic principles of investing and yet many investors, both professionals and laypersons, only put tiny portions of their equity/fixed-income allocations into EM, despite EM growth rates being double those of DM economies. Only in this year’s extreme scenario of a global low rate environment have investors piled into EM equities and debt. But even after retail inflows into EM corporate debt reached record levels this summer, a recent survey by JP Morgan revealed most are still underweight in EM debt. To see the benefits of adding EM to an investor’s portfolio, since 1999, the addition of EM IG & HY (to US credit holdings) have provided an extra 0.5% of return for the same level of risk, and dramatically higher returns for smaller increases in risk (see picture below).

I believe that the EM market is more resilient to crises than US and European markets. Why? Because DM markets are priced to perfection and any scandal or crisis can have wide-ranging negative effects for the whole DM markets. Just look at the most recent example, with problems at one bank (Deutsche Bank) shaking the European markets and even spilling over into the US.

In contrast, “EM” is truly diversified by 5 vastly different regions (Asia, Latin America, Middle East, East Europe, Africa) and over 40 countries within the broad corporate bond benchmark (no country more than 10% weighting). These include even advanced (but not yet officially “DM”) economies like Singapore, Taiwan, Hong Kong and Korea, along with riskier “high beta” countries like Russia, Turkey and South Africa. But it is rare for any individual crisis to affect the EM credit market as a whole.

When Turkey’s credit rating was junked recently, only the Turkish credits were weak. Last year, during 2015’s corporate and political scandals in Brazil, it was mainly Brazil’s markets that suffered. The prior year, in 2014, when Russia was in conflict with Ukraine, it was mainly Russia and Ukraine that were affected. During all of these events, regions like Asia continued chugging along with attractive returns, immune to the crises in other EM regions. Even for a more wide-ranging crisis, like when many commodities prices fell dramatically in late 2015 and early 2016, some countries suffered (LatAm, Middle East), while some countries benefited (Asia).

In 2016, EM credit markets have been the best in global fixed-income, with double-digit returns, in spite of a myriad of negative factors:

- still low commodity prices,

- slow turnarounds in Brazil and Russia,

- Turkish political problems and downgrade to junk,

- South Africa’s impending downgrade to junk,

- “China worries”,

- the Trump-Mexico effect,

- and the looming threat of a Fed rate hike.

I believe this is a testament to EM’s superior diversification, growth and ability to derive attractive long-term risk/return performance. This is something that cannot be ignored for long.